Budget 2024, Banks, and Market Cycles

Personal finance, investment philosophies and fun facts - all without the jargon.

Welcome to the seventh edition of the Bodhi Newsletter! In today’s edition, we cover:

An Explainer on the 2024 Union Budget

A Primer on Banking

What Every Investor Should Know About Market Cycles

Budget 2024 Explained

By Siddhant Goenka

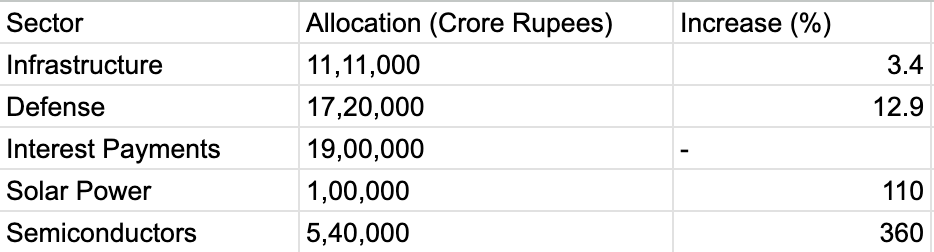

The Union Budget 2024 has unveiled a roadmap for India's economic growth, with significant allocations aimed at bolstering infrastructure, defence capabilities, and domestic manufacturing. Let's delve into some key data points to understand the budget's potential impact on various sectors.

Infrastructure Receives Record Investment

The budget allocates a whopping ₹11,11,000 crore (3.4% of GDP) towards infrastructure development. This substantial investment is expected to create a ripple effect, benefiting sectors like construction (₹11,11,000 crore), cement, steel, and transportation.

Defense Overhaul

Defence spending receives a significant boost, with a total allocation of ₹17,20,000 crore. This reflects the government's commitment to enhancing India's military preparedness and reducing reliance on defence imports. Notably, ₹23,800 crore has been earmarked for naval fleet modernization, presenting opportunities for domestic shipbuilding and allied industries.

Debt Repayment

The government aims to reduce the burden of interest payments, which currently stand at ₹19,00,000 crore. By lowering the fiscal deficit, the government hopes to bring down borrowing costs and free up resources for investments in other crucial sectors.

Renewable Energy Boost

The budget prioritizes clean energy transition with a substantial 110% increase in allocation for solar power, reaching ₹1,00,000 crore. This ambitious target presents lucrative investment opportunities in the solar energy sector and related technologies.

Focus on semiconductors

The government has introduced a modified program to develop a robust semiconductor and display manufacturing ecosystem in India. This initiative, with a massive 360% increase in allocation, signifies a strategic shift towards domestic production and reducing reliance on imports.

Skilling and Employment

The budget also emphasizes skill development and job creation. Significant allocations have been made for vocational training, apprenticeship programs, and digital skilling initiatives. The government aims to equip the youth with the necessary skills to participate in the growing economy. Additionally, the focus on infrastructure development is expected to generate employment opportunities across various sectors.

Rural Economy

The budget recognizes the importance of rural India and has allocated substantial funds for rural development programs. This includes increased spending on agriculture, irrigation, and rural electrification. The government aims to enhance the livelihood of rural populations and reduce rural-urban migration.

Taxation Changes

Budget 2024 also brought significant changes to the taxation of long-term capital gains (LTCG). A key alteration is the removal of indexation benefits for most assets. This means investors can either pay LTCG @ 12.5 % without adjusting the purchase price of an asset for inflation, or they can choose to stick with the old rules. While the LTCG tax rate has been reduced from 20% to 12.5%, the elimination of indexation can offset this benefit in many cases. This change is likely to impact real estate investors and those holding long-term equity investments significantly.

Investment Considerations

While the budget presents a promising outlook, investors should conduct thorough research and consider seeking professional advice before making investment decisions. The success of these initiatives hinges on effective implementation, and external factors can influence the overall economic landscape.

The Budget 2024 lays the foundation for India's economic transformation. With a focus on infrastructure, defense, manufacturing, skilling, and rural development, the government aims to create a self-reliant and inclusive economy. By aligning their portfolios with the government's vision, investors can potentially benefit from the long-term growth prospects of the Indian economy.

A Primer on Banking

By Soham Dengra

The Banking sector is one of the most important sectors in any country. However, despite their critical importance to a nation’s functioning, most people do not know how a bank actually functions. In this article, we’ll look at how a bank functions and certain terms one must understand while analysing a bank.

A bank is a lending institution which collects deposits from depositors and in return, it gives them interest on those deposits. The bank then uses these deposits to provide loans to borrowers at a higher rate than the deposits. The difference or the “spread” between these rates is pocketed by the bank as its profit.

Now that we know what a bank is, let's take a look at the 10 most essential terms one should know to analyse the banking sector:

CASA: This term refers to the bank's current and savings account deposits. These accounts are low interest-earning accounts which make them cheap sources of funds for any bank.

Term Deposits: Term deposits are deposits which have a fixed lock-in period before which they cannot be redeemed. At the same time, these deposits also offer the highest interest rates to the depositor and are, therefore, a more expensive source of funds for the bank. Term Deposits and CASA together form the majority of liabilities of a bank. Eg. FD and RD.

Advances: It refers to the loans given out by banks. Advances form the majority of the assets of a bank.

Net Interest Income(NII): This refers to the difference between the interest a bank earns from its advances and the interest it pays to its depositors. In a way, this can be seen as the Gross Profit of a bank. A higher NII means the bank earns significantly more from its loans than the amount it pays on its deposits, indicating better profitability. Often, the NII is calculated as a percentage of the total loans given out by the bank. This ratio is known as a bank’s Net Interest Margin (NIM).

GNPA: Non-performing assets refer to the loans which remain due and unpaid for over 90 days. These loans are doubtful to be repaid in the future and significantly impact a bank’s profitability and lending ability. A high NPA ratio is a sign of low asset quality and indicates poor lending ability. The sum of all the non-performing loans in a bank’s balance sheet is known as Gross Non-Performing Assets (GNPA).

Provisions: Each Bank must set aside a certain portion of their funds as assets to pay for potential losses in their loans in the future. These funds are known as provisions and act as a buffer for banks against any potential NPAs which they may face. They are a very accurate measure of the quality of a bank’s lending practices.

NNPA: Net Non-Performing Assets is the net difference between a bank’s GNPAs and provisions. Just like GNPA, a lower NNPA ratio is better for the bank and shows that the bank loans are not going bad.

ROA: Return on Assets (ROA) measures how profitable a bank is in relation to its total assets (loans). A higher RoA indicates that a bank is generating good profits from its lending operations.

ROE: Return on Equity (ROE) measures how efficiently the bank is using the funds from its shareholders to generate profit. A higher ROE indicates better profitability and vice versa.

Credit-Deposit Ratio: This is a ratio of a bank's total assets (loans) to its total liabilities (deposits). A CD ratio of 75% would mean that the bank is lending 75% of its deposits as loans. A higher ratio indicates that the bank is aggressively lending out its deposits and a low ratio is an indicator of slow or conservative lending.

Now that we know how to analyse a bank, in the next article, we will take a look at why Indian banking stocks are not doing well.

Riding the Market Waves: What Every Investor Should Know About Market Cycles

By Neel Issrani

As the Nifty continues to set new all-time highs, it might seem like the market is on an endless upward climb. However, understanding market cycles can help you navigate this journey with more confidence. These cycles are driven by a mix of economic factors, investor psychology, and global events. Historically, markets have swung between periods of growth and contraction, reflecting broader economic trends. Let’s take a closer look at these cycles, how long they last, and what returns you can expect.

The Four Phases of a Market Cycle:

1. Accumulation Phase: Typically following a market downturn, this phase sees savvy investors quietly buying as prices bottom out. Despite lingering pessimism, early signs of recovery, such as improving corporate earnings, may appear even if the headlines remain bleak. Bargains are often found here, but it requires patience and a contrarian mindset to capitalise.

2. Markup Phase: As more investors join in, confidence grows, and stock prices rise steadily. This phase is characterised by increasing stock prices, improving GDP growth, and positive earnings reports. Indicators like rising consumer confidence and declining unemployment rates often signal this phase. The market's momentum builds, with stock prices climbing steadily for years—this is where bull markets are born.

3. Distribution Phase: The market reaches its peak, and volatility sets in as investors begin to take profits. The market may not immediately decline, but caution is advisable as mixed signals and increased volatility start to emerge. This phase often signals the end of a bull market and precedes a downturn.

4. Downturn Phase: Declining stock prices and worsening economic conditions define this phase. Fear dominates, leading to sharp market value declines as investors rush to sell. Bear markets, though shorter than bull markets, are more intense, lasting about a year on average. However, these downturns typically reset the stage for the next cycle.

Historically, there are a few key trends regarding market cycles:

Bull Markets: These periods of rising prices tend to be longer and more rewarding than the bear markets that follow. Since 1962, bull markets have averaged about 51 months in duration, delivering substantial gains. For instance, the 1990s bull market lasted more than 12 years, with the S&P 500 returning an astonishing 582.1%, driven largely by the expansion of technology and internet companies.

Bear Markets: Although shorter in duration, bear markets can be more severe. The average bear market lasts just over a year but can see a significant drop in market value. The bear market following the 2008 financial crisis is a vivid example, where the S&P 500 lost nearly half its value in a matter of months. However, these downturns often pave the way for the next accumulation phase, setting the stage for recovery and future growth.

The contrasting durations and returns of bull and bear markets underscore the importance of maintaining a long-term perspective. While it's difficult to time the market and predict the exact duration of each phase, being aware of where the market is in its cycle can help guide investment decisions. Investors who remain disciplined and stay invested through these cycles are often rewarded with substantial long-term gains. The key is to remain patient, stick to your strategy, and avoid making impulsive decisions based on short-term market movements. With the right approach, you can ride the waves of the market and achieve your long-term financial goals

Sensex Showdown: Guess the Company

The company was founded in 1958 by Haveli Ram Gandhi who later sold it to Mr. Qimat Rai Gupta. The company manufactures various home and industrial appliances including fans, LED lights, switches, wiring etc. and is one of India’s leading electrical appliance manufacturers. It also owns brands like Lloyd, and Crabtree.