The Satyam Scam Explained, And The Impact of Budget 2025

Personal finance, investment philosophies and fun facts - all without the jargon.

Welcome to the thirteenth edition of the Bodhi Newsletter! In today’s edition, we cover:

The Satyam Scam Explained

Budget 2025 And Its Impact On Our Lives

The Satyam Scam Explained

By Shagun Khetan

Noticed those once-in-a-while AIC posters around campus? Something about…The Satyam saga…The Tech phoenix…?

Let’s break this down.

Satyam Computers, formed in 1987 in Hyderabad by Mr Ramalinga Raju, was once the crown jewel of the Indian IT services industry. The firm began with 20 employees(whom they called ‘associates’), rapidly becoming the country’s 4th largest company after TCS, Infosys and Wipro; operating in as many as 65 countries in the world. It was one of the first Indian IT companies to be listed on international exchanges like NYSE and EURONEXT.

But on 7 January 2009—

India and the global IT industry watched in horror as a letter written by B. Ramalinga Raju, confessing to orchestrating one of the biggest financial frauds in history, flashed on all news channels. Out of ₹5361 crores of cash and bank balances shown in the books, ₹5040 crores were non-existent. 18.5% of the debtors(~490 crores) were fictitious, 376 crores of accrued interest were false, and an understated liability of 1230 crores. Add the asset side(5040+490+376), and you get 5906 crores of bogus assets, matched by the exact amount of bogus reserves on the liabilities side. These bogus reserves were made by inflated billing; the Sep’08 quarter recorded a profit of 649 crores when it was in reality 61 crores. (the 24% shown, was in fact <3%).

Inflated billing, non-existent cash and bank balances, overstated debtors, understated liability—Satyam had quite literally tried everything.

But how did this start?

It’s believed to have started in the aftermath of 2000. The software industry had cracked the Y2K code, and Satyam was part of it. Subsequently, both revenue and profit dipped, and despite his best efforts to push delivery and billing, there was a gap between plan and performance. It was bound to impact the company’s rating in the market and lead to a sharp fall in stock price. Possibly this was when the idea occurred to Raju to bridge the gap with fictitious numbers. It’s also believed that he needed this to purchase acres of land in Andhra Pradesh amidst a booming realty market.

So to do this, Raju needed artificial billing to show Satyam was in the premier league. These fictitious invoices led to bogus debtors. But these debtors cannot stay outstanding for so long(in an audit, outstanding beyond 6 months is scrutinized), so he needed to show that he was getting money—which required him to fabricate bank statements to show a flow of money. Now this money had to be invested somewhere, which led to the creation of bogus fixed deposits. These deposits also showed fake interest income that was reflected in the asset side.

Usually, as an early warning sign of financial reporting fraud, investors look at the differences between cash flow and income closely. Since overstated revenues can’t be collected and understated expenses have to be paid, companies that misreport incomes often show a much stronger trend in earnings than in cash flow from operations. But Raju managed to manipulate cash flow too, as with the bogus fixed deposits. The Satyam scam was thus a stunningly and cleverly articulated comprehensive fraud, which went unnoticed by the SEBI, retail investors, external auditors, etc.

If everything was going so well, what triggered the confession?

Global financial crisis—2008. Satyam had cash flow issues and needed to raise money, but why should it need money when it had so much money in the bank? It was fake, but the bank didn’t know that, and so would raise suspicion if Satyam asked for money. Some vertical heads had also pointed out the turnover that was reflected in the audited statements was greater than what they had actually achieved. The Rajus had pledged their shares for borrowings as well, when their holdings were only 8%. As the share prices began descending in the wake of the global financial crisis, the lenders applied pressure for additional securities. The threat of an equity takeover was also stark since that would expose the gap. If outside agencies called out the fraud, the consequences could be devastating. America’s SEC would step in, he would be deported to the US for trial and taken away for a long time. Or maybe he wrote the confession so Satyam could survive. In the words of T.N. Manoharan, “I believe this version of ‘an inherently decent man who slipped on the righteous path’ when I read Raju’s giveaway line in his confession, ‘It was like riding a tiger, not knowing how to get off without being eaten.’”

Aftermath

The Indian government appointed a new board of directors to save the company, and to save the country’s reputation; after all, Satyam operated on a global scale, and such an event had tarnished the name of the country. The board proposed a revival plan, and the goal was to acquire a strategic investor post 100 days. On 13 April 2009, via a formal public auction process, a 31% stake in Satyam was purchased by Tech Mahindra, as part of its diversification strategy. Effective July 2009, Satyam rebranded its services under the new Mahindra management as “Mahindra Satyam”.

To learn more about the Satyam Scam and its ensuing turnaround in detail, make sure to attend the AIC speaker session hosted by none other than TN Manoharan- the man who turned around Satyam after the scam.

Budget 2025 And Its Impact On Our Lives

By Mahir Shah

The Union Budget of India is the annual financial plan of the Indian government. It outlays next year’s estimates of how much revenue is the government going to earn through tax and non-tax income and how much it is going to spend on different sectors like infrastructure, healthcare, defense, etc. The Finance Minister presents it every year in Parliament and it impacts everyone from job-seeking individuals like you and me to large corporations and industries. This year’s union budget was celebrated amongst many individuals and some popular investors too who were really impressed by it. So let’s look at some of the highlights from the Union Budget of 2025 presented a couple of weeks back.

Direct Taxation Reforms:

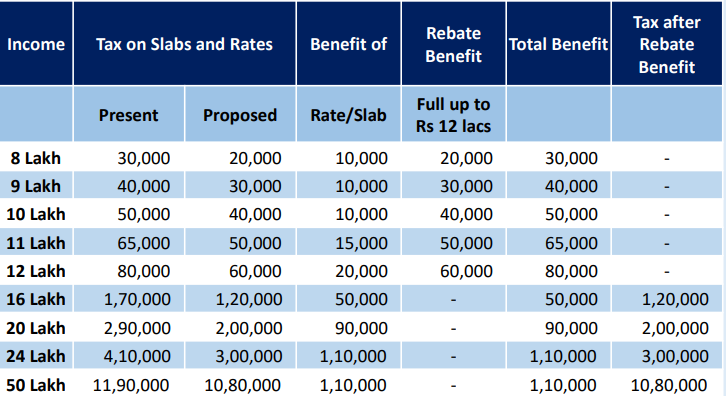

Below is the table comparing the tax slabs and rates of the previous year’s tax regime to the tax regime introduced this year.

According to the new tax regime, zero tax liability for personal income tax has been raised to Rs 12 lakh from the previous limit of Rs 7 lakh. The standard deduction for salaried employees has also been raised to 75000 from 50000, meaning that a salaried individual earning 12.75 lakh, will have to pay nil direct taxes.

Just to take an example, for an individual earning 30 lakhs of salary per annum, they will have to now pay approximately 4,75,800 in taxes and cess compared to 5,90,200 which they would earlier have to pay according to the old regime. That is approximately a 20% deduction in the total direct tax paid.

Below is a table summarizing the tax benefit an individual gets through the new tax regime:

What does this mean?

The government has decided to address the structural slowdown in consumption that the economy has been experiencing. The government is betting on the middle class to be the engine driving consumption growth, and the tax relief brought by the new tax regime will approximately release 1 lakh crore of purchasing power into the hands of the middle class.

However, on a closer look, we find that the majority of the benefits will fall on to the salaried individuals earning between 12 lakhs to 50 lakhs. Below is a table providing you with a summary of the effective tax rate across the slabs.

This bracket of individuals, who are slightly better-off consumers than the typical middle class, will benefit the most from the new tax regime in percentage terms. This bracket of individuals constitutes 20% of the total taxpayers in India and they will get 70% of the benefits from this new tax regime. This means that of the 1 lakh crore of tax benefit, 70,000 crore will flow to this 20% of taxpayers - roughly 7 million households. Therefore, this very encouraging stimulus has been targeted at certain demographic of income earners.

Therefore, this income tax relief will boost individual discretionary consumption rather than the consumption of staples or other necessary consumption goods. Therefore, this can lead to the revival of the automobile sector, the QSR industry and also drive growth for housing, tourism, aviation, and other sectors.

Increase in Capital Expenditure by the Government

Given the 1 lakh crore of tax benefit, there has been an overwhelming perception by all individuals that the government has opted for consumption at the cost of capital expenditure.

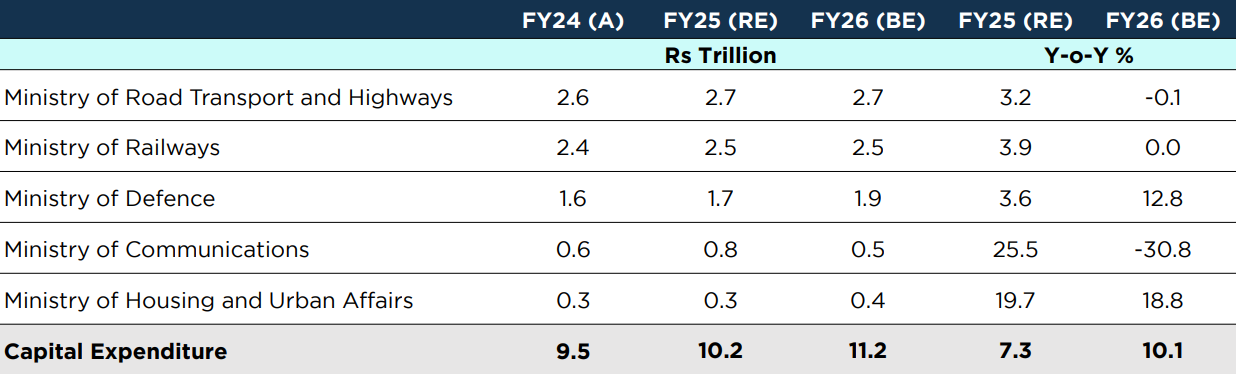

The table below provides a ministry-wise snapshot of the capital expenditure outlayed by the government and its comparison over the previous year’s budget.

The perception arises because the government’s capex is budgeted to rise by “only” 10.1% (y-o-y) to Rs 11.2 trillion in FY26.

The government’s capital expenditure is very crucial for the economic growth of a country as this funds the roads, infrastructure, education, and healthcare of the economy.

If that is the case, is the meagre 10.1% increase in the capital expenditure a cause for worry? Let's find out!

What does this mean?

Here, is a very important table to look at while forming a perception of the capex for the next financial year.

(In Rs Trillion)

The budget estimate of capex for FY25 was initially Rs.11.11 lakh crore, which was revised to Rs.10.18 lakh crore in this year’s budget (owing to the general elections) while the estimate for next year’s capex was estimated to be Rs.11.21 lakh crore.

If the government wants to achieve the revised estimate of capex, it has to spend a monthly average of Rs. 85000 crore. (10.2 lakh crore divided by 12 months)

Now, if we look at the actual capex done in the first 9 months of FY25 (April to December), it amounts to Rs.6.85 lakh crore. This translates to an actual monthly run rate of Rs.57000 crore. This lack of spending on capex can be attributed to the general elections held this year.

Therefore, if the government wants to achieve its revised estimate of capex, it needs to spend its balance capex of Rs.3.33 lakh crore over the next 3 months at a monthly run rate of Rs.1.11 lakh crore.

On top of this, the government has estimated the capex for FY26 to be at Rs.11.2 lakh crore at an average monthly run rate of Rs.93000 crore.

If we take the balance of this year’s capex spend and the next year’s estimate of capex, we come to a total amount of Rs.14.54 lakh crore which the government has to spend in the next 15 months (Jan’25-Mar’26). This would translate to an average monthly capex of Rs.97000 crore.

Therefore if you compare the actual monthly run rate of capex in the first nine months of the current year - Rs.57000 crore - with the estimated Rs.97000 crore of monthly average capex in the next 15 months, it tells you the real story.

Here we can see that the estimated monthly run rate for the next 15 months is significantly higher than the monthly run rate of FY19. So, we can say that the capex spending momentum will be reasonably strong and we can believe that the government is not doing a trade-off between consumption growth and capex outlay and the capex story is very much alive.

Fiscal Consolidation

The fiscal deficit for FY25 has been revised down to 4.8% of the GDP from budgeted 4.9% and the budget aims for a fiscal deficit of 4.4% of the GDP for FY26.

A fiscal deficit - the excess of government expenditures over its revenues - is typically funded through internal debts or borrowings from foreign institutions.

Therefore, this is good news for the economy as a lower fiscal deficit means that the government will borrow less to fund this deficit and maintain economic stability.

The budget is always a tradeoff between better fiscal discipline and higher growth. Being an emerging market and to become the third-largest economy in the next few years, higher growth should be desired.

However, the government estimates the fiscal deficit to come down to 4.4% of the GDP leading to fiscal consolidation.

What does this mean?

This fiscal discipline will pave the way for the RBI to loosen monetary policy and cut interest rates.

This can also lead to an improvement in the global credit ratings for India due to fiscal discipline and debt sustainability of India. Once India’s ratings improve, the overall cost of capital in the country could come down.

Therefore, the government is choosing a conservative path of reducing the fiscal deficit rather than increasing the borrowings to fund high growth rates.