Rupee Depreciation and Investment Learnings from Rakesh Jhunjhunwala's Right Hand Man

Personal finance, investment philosophies and fun facts - all without the jargon.

Welcome to the twelfth edition of the Bodhi Newsletter! In today’s edition, we cover:

Rupee Depreciation: Can it hit 90?

Utpal Sheth on Terminal Value Investing, Megatrends, and Gorilla Stocks

Rupee Depreciation: Can it hit 90?

By Shagun Khetan

“The rupee has depreciated over 3% in 2024, touching an intraday record low of 85.80/1$ dollar on 27 December, from 83.19/$1 at the start of the year.”

What exactly is rupee depreciation?

To define that, we need the concept of exchange rates—essentially the value of one currency in terms of another. So when the exchange rate is $1 = 80 Rs., it means to you need to pay 80 Rs. to buy a dollar. Rupee depreciation is when the rupee loses its value against another currency, in this case, the US dollar. When $1 = 85 Rs., you now have to pay a higher amount of rupees for the same value, meaning the rupee has weakened against the US dollar. The currencies are traded in the foreign exchange(forex) market and just like any other good, the exchange rate is determined by the demand and supply.

2024 has specifically seen a significant fall in the value of the rupee, most of which occurred in the last months of the year, post the Trump administration which had heightened the risk of aggressive import tariffs. When the rupee loses its value, imports become expensive, foreign education becomes costlier, people become apprehensive of their deposits, etc.

So why has this been happening?

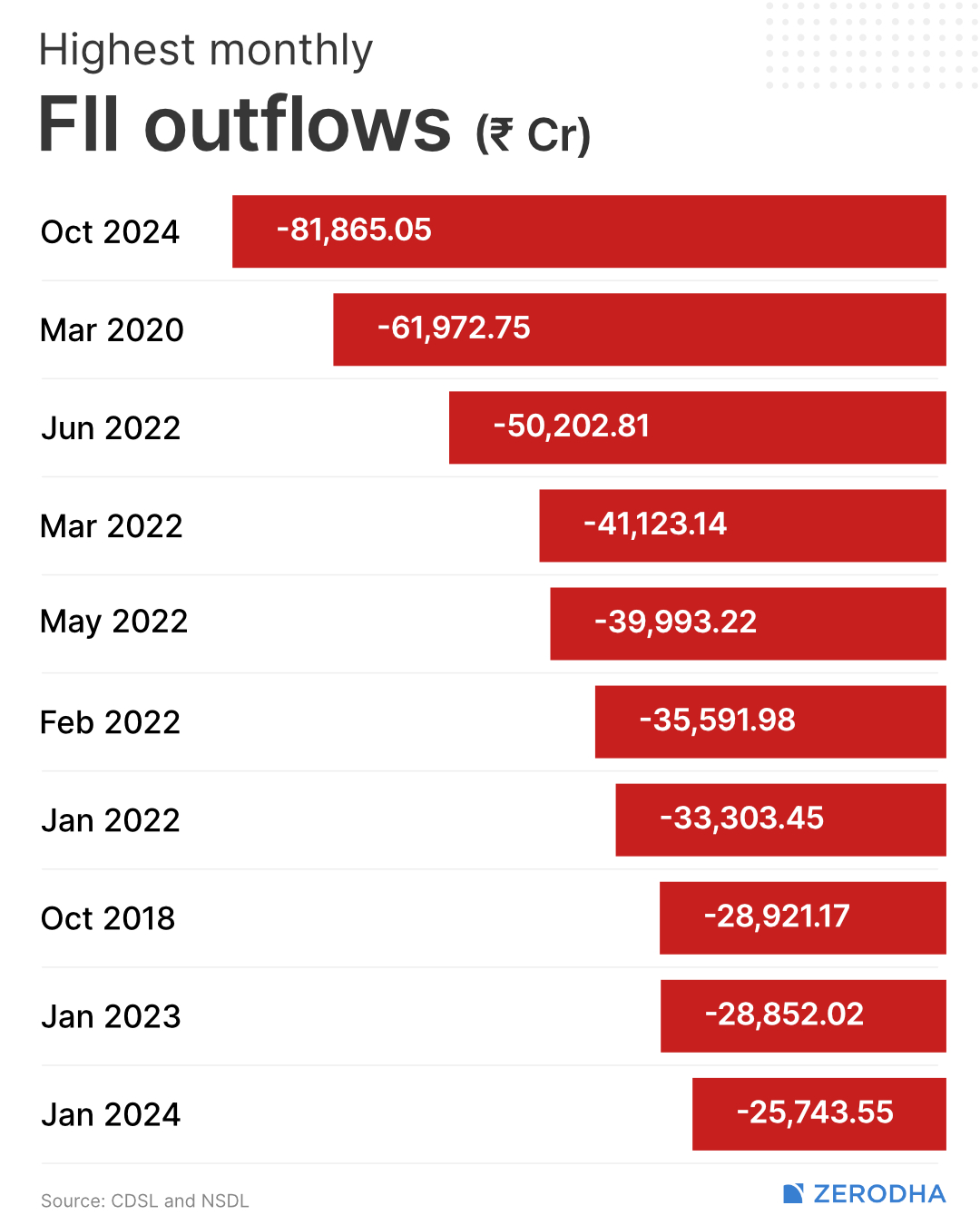

One reason is definitely the FII(Foreign Institutional Investment) outflows in the recent months. This affects the exchange rate as when foreign investors exit India, they demand dollars in exchange for the rupee, which weakens the domestic currency. High inflation in the aftermath of the coronavirus pandemic led to monetary tightening(increase in interest rates) by central banks which is now being reversed as inflation comes more under control. This has pushed overseas investors to withdraw money from India and invest in safer havens. The long-term trend of the rupee’s depreciation against the dollar is attributed to higher inflation in India than in the US due to the RBI’s looser monetary policy compared to the Federal Reserve.

Additionally, the widening trade deficit, caused by India’s traditional demand for high-value imports such as crude oil(prices of which are surging) and gold(which boosts demand for the dollar and thus weakens the rupee) and its inability to boost exports (which can help boost demand for the rupee) has also contributed to the lacklustre performance of the rupee. The RBI has been using its dollar reserves to cushion the rupee’s fall and minimize currency volatility by artificially increasing the supply of dollars in the forex market (and thus increasing the rupee demand). This has led to a fall in India’s forex reserves to an 8-month low of $630 billion as of the last week of January 2025 from over $700 billion in September 2024.

According to some analysts, the increased demand for the dollar is also due to the month-end dollar demand by importers settling bills in foreign currency (importers convert their rupees into dollars to pay for their bills at the end of the month) and the expiry of December currency futures and maturing positions in the outstanding forwards. These contracts are agreements between traders to buy or sell a specific asset(in this case, currency) at a predetermined exchange rate at a specific date in the future. Forward contracts are made over-the-counter and are settled only at the end of the contract while futures contracts are standardized to trade on stock exchanges and are settled daily. When these contracts mature, it involves the conversion of currencies which increases the demand for the dollar. Some analysts also argue that the depreciation is a result of the estimated overvaluation(about 8%) of the rupee relative to competing currencies.

What does the future hold for the rupee?

It seems as if the fate of the rupee is affected by what happens to the dollar, and now more than ever linked to the potential import tariffs by the Trump administration. India also imports almost 90% of the crude oil leading to a wider trade deficit, which means it needs to look at alternatives to mitigate revaluation risks. Analysts believe that the rupee depreciation would have been far worse if not for the RBI’s intervention to support the rupee against the dollar.

Investor Spotlight

Utpal Sheth on Terminal Value Investing, Megatrends, and Gorilla Stocks

By Mahir Shah

“Investing is an infinite game and you cannot play it with a finite mindset; learn to think long term.

- Utpal Sheth, Senior Partner and CEO at Rare Enterprises.

If you are inspired by the Late Rakesh Jhunjhunwala’s legendary moves and bets on companies in the market, chances are that Utpal Sheth was quietly pulling the strings behind the scenes. Fondly called Rakesh Jhunjhunwala’s right-hand man, the duo have cemented Rare Enterprises as one of India’s most iconic investment firms by identifying multi-baggers and delivering extraordinary returns. As the current Senior Partner and CEO of Rare Enterprises, he manages over $1bn of wealth.

He started his investing journey at ASK Financials at the age of 18 and then joined his father’s firm (his father - Hemendra Sheth - was one of the pioneers of equity research in India), after which he worked at the ENAM group before joining Rare Enterprises as CEO in 2003. He considers himself very fortunate to work with and be mentored by market legends like Mr. Asit Koticha at ASK, Mr. Vallabh Bhansali and Mr. Nemish Shah at ENAM, and the Late Rakesh Jhunjhunwala at Rare. Getting this opportunity to work with them, he not only learned a lot about financial markets and investing but also about people and life and having the right attitude.

Working in the markets right after giving his 12th-grade exams, investing has been a long journey for Mr Sheth, in which he developed a deep clarity of thinking and a knack for identifying multibaggers. Through this long journey, he has transitioned from the traditional approaches to investing which include value investing, growth investing, momentum investing, etc. to what he calls terminal value investing.

Terminal Value is the value of a company- its true potential and value- beyond the forecasted period for which future cash flows can be normally estimated. Therefore, terminal value investing is a dynamic way of looking at companies beyond financial analysis and recognizing the various sociological, economic, and cultural aspects at play, which have implications far beyond conventional financial analysis.

According to Utpal Sheth, an important precedent to terminal value investing is long-term investing. A long-term time frame is made up of many short-term time frames, and he believes that for one to be successful in terminal value investing, one has to be able to pass through these short-terms with a state of equanimity and be resilient during times of volatility, news headlines, and even times of negative returns. It all pays off in the long term so long as one is clear about the terminal value that one is pursuing.

However, he does not believe that one should buy and forget his investments for the sake of long-term investing. According to him, “forget it” is a luxury that investors do not have and he believes that while one is patient, one should not get complacent. The terminal value of a company is not static, it is dynamic. One should actively track the short-term and long-term factors that influence the fortunes and the terminal value of a company in which one has invested.

He also says that portfolio management is key to having successful results. You cannot say that you have belief in a company that you think is the best stock in the country and then only give 1% of weight to it in your portfolio. Only by having courage and giving weight to your convictions, assuming the fundamentals are strong, can one experience a very significant material return on their investments. Diversifying is the best hedge against market and company-specific risks but wealth is not created by giving minimal weight to your convictions.

How to identify multi-baggers?

Utpal Sheth believes that to identify multi-baggers one should look at 3 crucial aspects in a company which are the largest determinants of value creation:

Participation in megatrends.

Leadership capabilities.

Intangibles.

What are megatrends?

A megatrend is a structural change in the economy. Megatrends are transformative forces that reshape economies, drive innovation, and redefine business models. They transcend geographies, generations, and governments. Moreover, they are sustainable. They persist over 2-3 decades and create paradigm shifts. They have non-linear growth and irreversible consequences. One example of a megatrend is the IT revolution in India which started in the early 90s and is still persisting.

Below is how the IT index fared compared to the Nifty 50 simultaneously:

From this, we can make out another important aspect of megatrends; they consistently outperform the market and are not mean-reverting. When a company is participating in a megatrend, it means that it has a long runway of growth and can service a large market.

After identifying a megatrend, one should focus on the companies with leadership capabilities that have the right business model and that have some competitive advantage or ‘moat’ in that chosen space. In this way, the company will be able to make the most of the large addressable market and the long runway of growth.

However, both these factors - megatrends and leadership capabilities - will not be meaningful if they are not sustainable. The sustainability is caused by the internal factors of the company - the intangibles. The intangibles are assets that a company owns that are not factories or buildings, but they are assets like the quality of management that they have, the practices that they follow, the kind of risk management that they have inculcated, the brands they have built, etc.

According to Utpal Sheth, these 3 factors contribute the most to the terminal value of the company. If a company has 1 or 2 of these factors in place, it can work out but it will run out of steam after a few years. It is a very rare coincidence to find a company that possesses all three qualities. Mr. Sheth refers to these companies as gorilla stocks.

By making a comparison of gorillas with monkeys in the jungle, Mr Sheth is trying to demonstrate the difference between multi-bagger stocks with other stocks. By referring to the attributes of gorillas in the jungle, he is trying to reflect the attributes of multi-bagger stocks in the financial markets.

There are many monkeys in the jungle but very few gorillas - they are rare.

Gorillas are outsized as compared to monkeys - they are dominant.

Gorillas are not challenged by the monkeys - they have sustainable moats.

Gorillas have a lifespan double that of monkeys - longevity.

According to him, one has to find the right jungle (the right megatrend) and find the right gorilla in it (the multi-bagger) to compound their wealth in the long term.

He advises creating a portfolio around these gorilla stocks by focusing on 3-4 megatrends in which one has a strong conviction and in each megatrend focusing on 2-3 players who have leadership qualities. One can classify these players as 1) clear leaders, 2) near leaders, and 3) emerging leaders. By having a portfolio of 12-15 stocks with high convictions, one will find that a few stocks which they thought were gorillas will turn out to be monkeys and that is okay. The other stocks which actually turn out to be gorillas will become multi-baggers for the investors and create generational wealth for them.

Utpal Sheth has used this strategy and created enormous wealth for himself and his clients by having strong bets on companies like Titan, CRISIL, and Shree Cement among others.

Currently, along with working at Rare Enterprises as CEO, he is also the mentor for the TRUST group and regularly appears for interviews, seminars and talks to educate and inspire fellow investors and young minds. He is like a walking encyclopedia of market wisdom and is highly respected even amongst the best investors in the market.