Ramesh Damani's Legacy, India's Family Office Revolution, and Buffett on Risk and Volatility

Personal finance, investment philosophies and fun facts - all without the jargon.

Welcome to the fourteenth edition of the Bodhi Newsletter! In today’s edition, we cover:

Ramesh Damani – The Oracle of Dalal Street

The Family Office Revolution in India: Transforming Wealth Management

Buffett On Risk Vs Volatility

Investor Spotlight

Ramesh Damani – The Oracle of Dalal Street

By Malhar Sanghavi

Mr.Ramesh Damani is one of the well-known faces of the investing community in India. He has helped popularize equity culture in the country through his popular TV show Wizards of Dalal Street and various talks in India’s Business and undergraduate schools. A very successful investor who is known for investing in good businesses at reasonable valuations, he is also the Ex-Chairman of Avenue Supermarts Ltd (Dmart).

Ramesh Damani started investing in the markets once his father challenged him to invest $10,000 in the 1980s. During a euphoric bull run in the United States, he lost the entire amount. This event sparked Damani's deep-seated interest in the intricacies of the stock market. Little did he know that this setback would be the catalyst for a lifetime of learning and success.

Damani’s investment philosophy is based on a fundamental principle: choosing the right industry. He meticulously studies market trends, identifying sectors poised for growth and innovation. It's within these fertile grounds that Damani seeks out potential investments. One of his standout successes, Infosys, is a shining example of this approach. In the burgeoning IT industry of the 1980s, Damani was the first to recognise the immense potential of the IT companies because of his background in USA companies and invested in Infosys which went up by 100x in just a few years.

Mr. Damani picked out the PSU bull run in India perfectly by taking a large bet on the public sector companies in India since 2018 and they have delivered fantastic returns for him. He believes in catching the leaders of the bull market early and that is exactly what he did. Mr. Damani’s biggest regret in investing is not backing up the truck on his best ideas; even though he picked the right stocks he did not make sizable money on them. He has learnt from his mistakes and backed up the truck on the PSU trade.

However, Mr. Damani is not immune to failures. He invested in MTNL with a great vision for the company which eventually did not pan out. MTNL, once a telecommunications powerhouse, faced a steady decline under the shadow of changing government policies. The policies implemented under the National Democratic Alliance and United Progressive Alliance favoured private companies. Then, with the uptrend of 3G and 4G, MTNL started losing market share to private companies and were not able to compete because of bad customer experience as a result of being a monopoly in the industry for the past decade. Mr. Damani did not expect this kind of disruption in the industry and was late to exit his investment.

He is extremely humble even after creating such a vast fortune from investing, and still has the drive to learn and improve. He enjoys mentoring budding investors and frequently talks to young students and guides them in their journey. The one advice he gives everyone is to read as much as possible and he advocates reading about various topics which he thinks will eventually shape you as an investor and a person. Rameshji’s guiding rule to know if he is doing okay in the markets is the principle of doubling portfolios every three years, equivalent to a 24% Compound Annual Growth Rate (CAGR), which leads to a 1000x return over 30 years.

Rameshji mentions that he has learnt the most from Mr. Chandrakant Sampat, Mr. Radhakishan Damani and the late Mr. Rakesh Jhunjhunwala. He has alluded his success many times to the group of friends he was part of; even though they all made money in different companies they had one thing in common which was- They were always bullish on India.

For me Rameshji is the best investor in the country not just for his stock picking and knowledge about the markets but because he is so passionate and humble that he shares his wisdom with youngsters like us. I think the Indian stock market rests on the back of 3 R’s- Rakesh, Radhakishan & Ramesh which stand for Returns, Resilience & Robustness.

To learn more about his investing journey and philosophy, make sure to attend AIC’s speaker session this Saturday, 1st March 2025 @ 1:30 pm- and get a chance to meet the legendary investor in person!

The Family Office Revolution in India: Transforming Wealth Management

By Neel Issrani

In the world of investing, the spotlight often falls on institutional heavyweights like FIIs, mutual funds, pension funds, and private equity firms. Meanwhile, retail investors are celebrated for their growing presence in markets. Yet, a quieter but powerful player has been making waves in the financial ecosystem: family offices. These private wealth management entities, tailored to ultra-high-net-worth individuals (UHNWIs), have been rapidly gaining traction in India. In just six years, the number of family offices in India has skyrocketed from 45 in 2018 to over 300 today, managing an estimated $30 billion in assets. These entities are not just reshaping how the wealthy manage their portfolios—they are actively driving innovation, supporting startups, and influencing markets in ways that were once the domain of institutional investors.

A family office goes beyond traditional wealth management, offering comprehensive services that include tax planning, estate management, philanthropy, and even concierge-like personal services. Unlike traditional investment firms bound by strict mandates, family offices are more agile, allowing them to invest in diverse sectors and take risks that align with their unique philosophies. For example, PremjiInvest, the family office of Azim Premji, has been instrumental in funding high-growth sectors like technology and consumer goods, with investments in companies like Flipkart and FabIndia. Similarly, Narayana Murthy’s Catamaran Ventures has backed startups like BigBasket and Cure.fit, nurturing India’s entrepreneurial ecosystem and demonstrating the ability of family offices to act as incubators of change.

India’s economic growth has created an unprecedented surge in wealth, especially among first-generation entrepreneurs. Liquidity events like IPOs or acquisitions have provided these entrepreneurs with vast sums of wealth, prompting the need for sophisticated management solutions. Family offices fill this gap by offering a personalized approach that goes beyond financial returns to include legacy building, succession planning, and philanthropy. The Burman Family Office, which manages the wealth of the Dabur promoters, channels funds into private equity and venture capital while actively supporting philanthropic causes in healthcare and education. For these families, a family office isn’t just a financial tool—it’s a statement of purpose, aligning wealth with long-term vision and values.

What sets family offices apart is their ability to invest directly in private equity, real estate, and alternative assets. Over 40% of family office portfolios in India are now allocated to these high-growth areas, enabling them to deliver superior returns compared to traditional investments. For instance, RNT Associates, Ratan Tata’s family office, has invested in a diverse range of sectors, from med-tech startups to renewable energy, reflecting a commitment to both profit and progress. This direct investment approach also allows family offices to bypass intermediaries, reducing costs and enhancing control over their financial decisions.

Another unique aspect of family offices is their focus on social impact, sustainability and ESG principles. Unlike many institutional investors, family offices often have the freedom to prioritise impact over immediate financial returns. The Tata family’s investments in rural healthcare and renewable energy projects demonstrate how wealth can be used as a force for good. These investments are not just financially rewarding but also socially transformative, creating a lasting legacy for future generations.

While family offices have traditionally been concentrated in metropolitan hubs like Mumbai, Delhi, and Bengaluru, they are now expanding into Tier-II and Tier-III cities. Wealthy promoters in cities like Ahmedabad and Coimbatore are establishing family offices, reflecting a broader acceptance and need for structured wealth management across the country. This geographical expansion is democratizing access to sophisticated financial tools, making family offices an essential component of India’s evolving financial ecosystem.

Despite their growing influence, family offices operate under the radar, often overshadowed by institutional and retail investors. Yet their contributions to the financial landscape are profound. By funding early-stage startups, supporting large-scale projects, and co-investing with private equity firms, family offices are reshaping markets. Their ability to operate flexibly and align wealth with purpose makes them indispensable players in fostering innovation and sustainable growth.

Buffett On Risk Vs Volatility

By Soham Dengra

Many of us tend to use the words “risk” and “volatility” quite interchangeably while talking about investing. However, we could not be more mistaken in doing so. Warren Buffett himself has been a very ardent advocate of differentiating volatility- often called “beta”- from risk, and has emphasised their critical distinction many times in his famed shareholder letters (a must-read for anyone interested in investing).

Volatility is not risk:

Simply put, volatility measures the price fluctuations of an asset over a period of time. While it can create emotional distress for investors, Buffett argues that volatility does not inherently equate to risk. Risk, in Buffett's words, is “the probability of an investment causing a loss of purchasing power over the holding period.”

For instance, while stocks may have high “beta” and experience significant volatility in the short term, they are still highly likely to deliver inflation-beating returns in the long run. Conversely, stable and “safe” investments in instruments like currencies, bonds and FDs might show minimal volatility but fail to outpace inflation, leading to a real loss of purchasing power—a risk Buffett deems far more significant for any investor.

Here’s what Buffett says about beta and risk in one of his famed annual letters:

The Pitfalls of Equating Volatility with Risk:

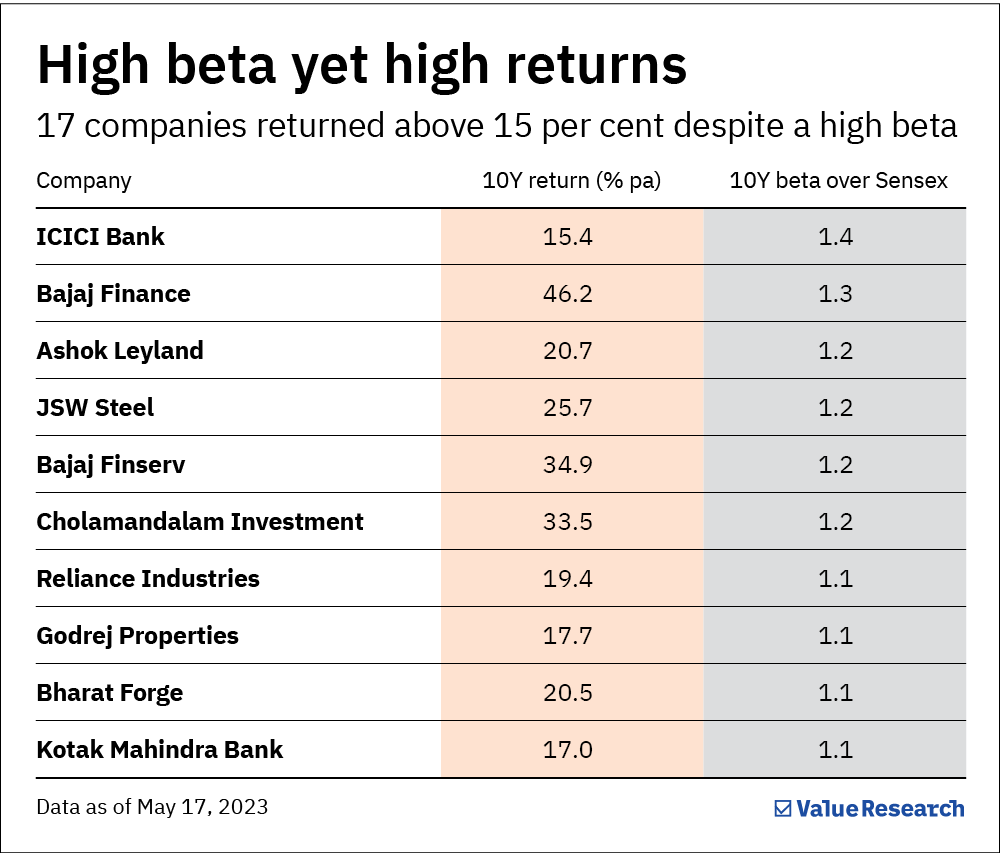

Traditional finance often uses beta, a measure of volatility relative to the market, as a proxy for risk (A beta of 1 indicates that a stock is as volatile as the benchmark index). Buffett dismisses this approach as being overly simplistic and misleading. He argues that focusing solely on beta can cause investors to overlook high-quality opportunities in temporarily distressed markets or industries.

For example, during market downturns, an investor who is overly concerned with beta might shy away from purchasing undervalued stocks due to their high short-term volatility. This behaviour, often driven by fear of price swings, may result in missed opportunities for long-term wealth creation.

Buffett has often used volatility in the markets as an opportunity to purchase great businesses at bargain prices. For example, during the 2008 financial crisis, Buffett seized opportunities to invest in distressed companies by purchasing $5 billion worth of Goldman Sachs preferred shares and $5 billion in Bank of America at the height of the Global Financial Crisis. These deals, struck when others panicked, turned into some of Berkshire Hathaway’s most lucrative investments, demonstrating that volatility often presents opportunities rather than risks- when viewed in conjunction with a solid investment strategy.

Real Risk: Permanent Capital Loss

Buffett believes there is only one true risk- the permanent loss of capital. He quips “Bonds promoted as offering risk-free returns are now priced to deliver return-free risk”. This is because while bonds might appear safe due to their stable returns, their inability to deliver inflation-adjusted post-tax gains makes them risky despite their low volatility. Similarly, Buffett also criticizes investments in gold, arguing that it relies on speculative demand rather than intrinsic value.

In contrast, Buffett supports productive assets like stocks, businesses, and farmland, as these assets generate income and appreciate over time- making them safer choices for long-term investors despite potential short-term price fluctuations.

Even in the Indian context, embracing volatility has yielded immense returns for patient investors with sound investment theses. For instance, the Sensex dropped nearly 40% during the 2008 crisis but rebounded to deliver extraordinary returns over the subsequent decade. Similarly, the Indian markets saw steep corrections in early 2020 but went on to rally sharply as the economic recovery gained momentum.

Lessons for Investors:

Buffett’s approach offers practical strategies for managing risk

Buy During Volatility: Times of panic, like the 2008 crisis, create opportunities to acquire high-quality assets at discounted prices.

Think Long Term: Short-term price declines are opportunities, not threats, as long as the fundamentals remain sound.

Focus on Fundamentals: Evaluate a business’s intrinsic value and its ability to grow purchasing power rather than reacting to market noise.