Learnings from the IL&FS Crisis, Effect of Big IPOs, and SGBs Decoded

Personal finance, investment philosophies and fun facts - all without the jargon.

Welcome to the eleventh edition of the Bodhi Newsletter! In today’s edition, we cover:

Sovereign Gold Bonds: A Modern Investment in Tradition

Do Big IPOs signal the end of a short-term Bull Run?

What Retail Investors Can Learn from the IL&FS Crisis

Sovereign Gold Bonds: A Modern Investment in Tradition

By Dersh Savla

What are Sovereign Gold Bonds?

Sovereign Gold Bonds (SGBs), introduced by the Government of India, offer a secure and innovative way to invest in gold. Issued by the Reserve Bank of India (RBI), these bonds allow investors to gain exposure to investments in gold without the challenges of physical ownership. SGBs are provided for a tenure of eight years with an exit option after five years, investors gain a fixed annual interest rate of 2.5%, paid semi-annually, and the maturity value is based on prevailing gold prices. These bonds are priced according to the market value of 999-purity gold, as determined by the India Bullion and Jewellers Association (IBJA).

The Gold Rush in 2024

Gold has posted exceptional returns in 2024, driven by several factors. Geopolitical risks including the Middle East tension and the Russia-Ukraine war, have spurred the demand for gold which acts as a safe haven in times of uncertainties. Additionally, central banks have also increased their gold holdings, further driving up the price. Lastly, the recent cuts in US Federal Reserve interest rates have made gold more attractive by lowering the opportunity cost of holding bullion. These factors have also led to experts forecasting that gold may continue its upward trajectory in 2025 as well. Analysts have also predicted a similar rally in 2025 for gold as seen in 2024, however, it is all dependent in geopolitical developments. UBS forecasts the price of gold reaching $2900/oz by the end of 2025, while Citi, Goldman Sachs and JP Morgan are eyeing a target of $3000/oz (Currently, the price is around $2626.78/oz). This highlights how uncertainty with speculation has been driving the price of gold in a positive frenzy.

Why are SGBs a Preferred Investment?

SGBs offer a fixed return through interest and capital appreciation as gold prices have been increasing. This dual benefit makes them attractive to investors seeking steady income and long–term growth in wealth. Secondly, unlike physical gold, SGBs incur no storage or security expenses, this eliminates risks associated with theft or purity concerns, offering a hassle-free investment. Moreover, SGB owners are exempted from capital gains tax upon maturity and investors can avail of indexation benefits if they transfer the bonds. These benefits make SGBs highly appealing for long-term financial planning.

Why did the government launch SGBs?

India’s insatiable demand for gold strains the country’s current account balance, given the high volume of imports. By promoting SGBs the government aimed at shifting investments from physical gold to financial assets, supporting economic growth and reducing the foreign exchange outflows. Investors, in turn, benefited from a modernised approach to owning gold while indirectly contributing to national economic priorities.

However, the government is reconsidering the viability of the scheme due to the high fiscal cost coupled with the recent reduction in import duties on gold, which has led to the government reassessing the scheme’s effectiveness. The scheme has thus seen a reduction in issuance frequency over the years, with the number of tranches declining from ten to four to now just two per year. This reduction reflects the government’s changing stance on SGBs, driven by its priorities of maintaining fiscal stability. Even though the Budget presented on July 23, 2024, stated the reduction of gross SGB issuances from Rs. 29,638 Crore to Rs. 18500 Crore, no issuances of SGBs have been made so far, in the current financial year of 2024-25.

Do Big IPOs signal the end of a short-term Bull Run?

By Rajit Mundhra

Big IPOs or a surge of multiple IPOs hitting the market at once can often signal a short-term market downturn or a selling trend. This happens because a significant amount of money is pulled from the stock market (secondary market) as investors redirect their funds to apply for new IPOs in the primary market.

Major IPOs often require substantial capital leading investors to often sell off their existing stocks to gather the necessary funds. This sudden selling spree can reduce the overall buying power in the market. Since IPOs are frequently oversubscribed, large sums of money get locked up for several days, further draining the market's liquidity. This can be especially problematic when the market is either on a bull run or trying to stabilize after a decline.

The financial impact of these large IPOs can be significant. For instance, IPOs can draw anywhere between ₹5,000 crores to ₹50,000 crores from the secondary market. This leads to reduced demand for existing shares, increased selling pressure and short-term market dips.

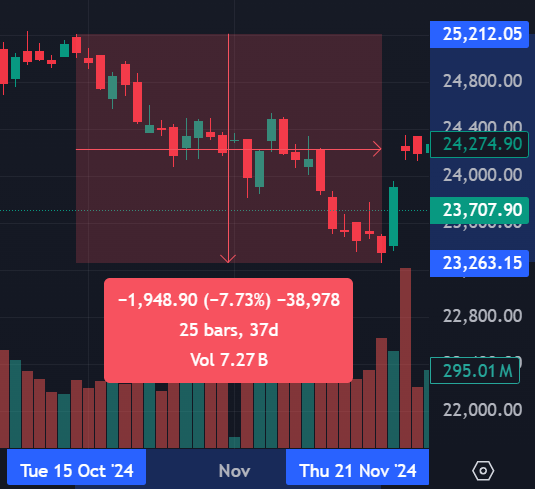

Take the recent example of the Hyundai India IPO, the largest in India. The company aimed to raise around ₹28,000 crores, but due to the massive hype and oversubscription (2.37 times the offered amount), ₹66,000 crores were locked up in the secondary market for a week. This significant cash drain reduced buying power and increased selling pressure, contributing to an immediate temporary market dip.

Proving this thesis- The Hyundai IPO opened on 15th October and that is the day when The Nifty50 (NSE's benchmark index) last touched 25200 points. The index subsequently fell almost 8% in the next 30 days to reach 23250 points. There are several such instances that help prove this thesis. 9 mainboard IPOs opened between 19th and 23rd December 2024. The Sensex (BSE's benchmark index) plunged more than 5% in that week itself.

NIFTY 50:

SENSEX:

While IPOs often indicate market confidence and growth, an influx of multiple large IPOs at the same time can disrupt market stability. A bigger concern is that these significant applications block investors’ money for a week thereby undermining a secondary market rally. Mayank Khemka, India at Deutsche Bank, mentions that "Primary market activity is linked to the secondary market rally and many IPOs often occur during the later stage of a bull market." He thereby says that a large number of IPOs lead to a fall in the secondary market usually hinting ats the end of a Bull run.

We shall also see many major IPOs in 2025 like Reliance Jio, LG and Flipkart. Investors should exercise caution during such periods as the market may experience short-term volatility. Investors can also look at these periods in advance to plan their investments accordingly and get comparatively cheaper valuations. At the same time, traders can use this as a great opportunity for a 'short' position.

What Retail Investors Can Learn from the IL&FS Crisis

By Heet Dhawale

The Infrastructure Leasing & Financial Services (IL&FS) crisis of 2018 stands as a pivotal event in India's financial history, offering crucial lessons for retail investors. Established in 1987, IL&FS was a prominent infrastructure development and finance company in India, operating through more than 250 subsidiaries across various sectors, including transportation, energy, and finance.

The company played a significant role in financing and developing major infrastructure projects nationwide including the 9-km Chenani-Nashri tunnel (India’s longest road tunnel), Delhi-Noida Toll Bridge, Tripura Power Project, and Gujarat International Finance Tech City (GIFT).

IL&FS's financial troubles were exacerbated by operational challenges. Active projects faced cost overruns due to delays in land acquisition and obtaining necessary permissions, while new infrastructure projects came to a standstill.

The IL&FS crisis affected various sectors, including mutual funds and non-banking financial companies (NBFCs), leading to significant losses for investors with heavy exposure to these areas. This highlights how concentrated investments in a single company or sector can amplify risks. Diversifying investments across different asset classes and sectors can mitigate such risks. During the crisis, the bankruptcy cases wiped out Rs.8.48 lakh crore of investor’s wealth while Sensex shed 2,000 points just in a week, sparking a bloodbath in the market.

The IL&FS debacle underscores the necessity for investors to conduct thorough research before committing funds. Understanding a company's financial health, debt levels, and business model is crucial. Relying solely on credit ratings or market reputation can be misleading, as evidenced by IL&FS's high credit ratings shortly before its collapse. (Rating agency ICRA downgraded the ratings of its short-term and long-term borrowing programs from “AAA” to “D” only after the crisis emerged.)

Investors must recognize that debt instruments, while often perceived as safer than equities, carry inherent credit risks. The IL&FS default led to a reevaluation of credit risk assessments, emphasizing the importance of scrutinizing the creditworthiness of issuers beyond surface-level indicators.

The crisis also brought to light the regulatory gaps concerning NBFCs, which, unlike traditional banks, were not subject to stringent Reserve Bank of India (RBI) oversight. In response, the RBI intensified its monitoring, particularly focusing on the top 50 NBFCs that constitute 75% of the sector. This development emphasizes the evolving regulatory landscape and the need for investors to stay informed about regulatory changes affecting their investments.

Additionally, the arrest of IL&FS's former vice-chairman, Hari Sankaran, by the Serious Fraud Investigation Office (SFIO) for sanctioning loans to non-creditworthy entities highlights the legal consequences of corporate mismanagement. Therefore, investing in companies with transparent and ethical management practices to reduce exposure to corporate fraud and mismanagement becomes highly critical for a retail investor. This aspect can make or break the company and a deep study and recognition of their reputation is necessary.

The IL&FS crisis brings to the forefront the importance of due diligence, diversification, and scepticism towards credit ratings for retail investors. It highlights the need for regulatory vigilance and robust corporate governance. By learning from this debacle, we investors can make more informed decisions, better assess risks, and contribute to a more stable financial ecosystem. Recently, the group discharged a debt of Rs 38,082 crore to creditors on 30 September 2024. Due to various measures taken by the new board, IL&FS says its overall debt resolution across the group is estimated to reach 61.39% or Rs61,000 crore of its total external debt outstanding of Rs 99,355 crore.