Investing 101: Mutual Funds, Gold and Fundamental Analysis (+ fun facts!)

Personal finance, investment philosophies and fun facts - all without the jargon.

Welcome to the second edition of the Bodhi Newsletter! In today’s edition, we cover:

Mutual Funds

Gold — The Obsession, and how to invest in it

Investor Spotlight: Ramesh Damani

Fundamental Analysis 101: Key Ratios

Fact of the Day: Asia’s Oldest Stock Exchange

Personal Finance

Mutual Funds: The Ice Cream Sundae of Investing

By Subham Sen

In an age where ads seem to be getting more and more difficult to skip, you've probably found it hard to overlook those ‘Mutual Funds...Sahi Hai’ commercials. For a lot of people, mutual funds (MFs) are the first step into the world of investing. They are simple, straightforward, versatile, and can be quite rewarding. Investing in mutual funds as a first step is like getting an ice cream sundae instead of plain vanilla ice cream – you get your chocolate and vanilla ice cream (blue chip stocks), as well as some more interesting stuff like waffles, sprinkles, cherries (small cap, midcap, value picks, etc).

Stocks versus Mutual Funds – The Basic Difference

What’s the difference between buying a stock and investing in a mutual fund? When you buy a stock, you put your money into one company and get a share of its ownership. But when you invest in a mutual fund, you’re not doing it alone, and there’s more than one stock – you’re basically a group of people pooling your money to invest in a bunch of stocks. The benefit of this is that for the same amount of money, you can invest in a bunch of companies instead of just one, and even if the stock prices of a few companies go down, the others will likely go up or stay the same (i.e, what we call the diversification benefit).

In contrast to stocks, mutual funds use a different term for market price – they refer to it as the Net Asset Value per unit or NAV per unit. To simplify NAV, and given our frequent use of food analogies throughout this article, imagine the mutual fund as a pizza. The NAV per unit is the price of one slice. As the individual securities within the fund appreciate or depreciate in value, so does the NAV. It's your guide to see how your investment is doing. Watching it rise is like seeing your pizza slice getting bigger over time! NAV per unit is like a mutual fund's heartbeat. It tells you the value of each unit or share in the fund. Technically, it is the market value of the financial assets held by the mutual fund divided by units of that fund. The NAV changes daily after the markets where the fund's assets are traded close. It depends on how the assets' prices ended for that day.

How to invest in a mutual fund?

In India, you can invest in mutual funds if you have a PAN Card (provided by the Income Tax Department) and a bank account.

There are two primary avenues for investment – one is a lump-sum investment, and the other is through SIPs (Systematic Investment Plans). Lump-sum investments involve putting a substantial amount of money into a MF all at once. On the other hand, SIPs allow you to invest smaller, regular amounts at scheduled intervals, typically monthly. SIPs are favoured by both employed individuals and students because they require a smaller initial investment, involve lower risk and promote the development of a consistent saving habit. Both investment approaches possess their own set of merits and drawbacks, which we will explore in more detail in upcoming newsletter editions.

If you search 'mutual funds in India' online, you'll come across terms like direct, regular, hybrid, debt, index funds, 'digital India fund,' 'sustainable energy fund,' and more. Moreover, numerous fund houses offer these options; some of the prominent ones include SBI MF, ICICI Prudential MF, HDFC MF, and Nippon India MF. While these might sound hopelessly daunting right now, rest assured that upcoming editions of the Bodhi newsletter will cover these topics. We'll explore these fund types, demystify the jargon, and provide valuable tips for making informed mutual fund investments. Stay tuned for a wealth of financial knowledge!

The Sona Saga: Exploring India’s Love Affair with Gold

By Rishika Jain

With a whopping 21,000 tonnes in their treasure troves, Indians proudly hold the crown for being the world's largest holders of this precious metal. But hey, it's not just for show! Gold has become the ultimate BFF of Indian investors, offering financial growth, stability, and a touch of diversification to their portfolios.

Why the obsession with gold?

The Lineage Factor: Gold is not just an investment; it's a part of cultural traditions and family legacies, passed down from generation to generation. The sentimental value of gold assets in India can be understood from the statistic that Indian women alone hold 11% of the world’s gold, largely in the form of ‘idle’ jewellery.

Performance during Economic Crises: Gold is a safer asset class during economic uncertainty, as demonstrated by its positive performance during the 2008 global financial crisis. In fact, much of the increase in the price has happened post 2008. Between 2001 and 2008, gold prices in India were only ₹12,500 per 10 gm!

What’s the catch?

Gold lacks intrinsic value, relying entirely on market sentiment for its worth, making it less stable than assets like real estate or businesses. Storing physical gold securely is difficult, and unlike stocks or bonds that offer regular income through dividends or interest, gold does not generate periodic earnings.

In light of these limitations, considering alternative investment strategies like Gold ETFs or Sovereign Gold Bonds can offer greater convenience, liquidity, and potentially more stable returns for modern investors:

1. Sovereign Gold Bonds (SGB)

One way to invest in gold is through Sovereign Gold Bonds. You can purchase them during subscription periods, through various channels like scheduled banks, post offices, stock exchanges, and online platforms. They have a minimum and maximum investment limit specific to the issuance, as shown in the following figure. They offer an interest at the rate of 2.5% per year payable half-yearly on the nominal value of the bond. However, SGBs come with the limitation of fixed tenure, which might affect your liquidity.

2. Gold ETFs

Gold Exchange-Traded Funds (ETFs) are a modern and convenient way to enter the gold market. These are mutual fund schemes that invest in physical gold and other gold-related assets, and they are traded on stock exchanges, much like stocks themselves. Investing in Gold ETFs offers diversification and the expertise of professional management. In India, most banks offer Gold ETFs. Below is a list of the largest ETFs in India and the parameters they are judged on:

3. Digital Gold

Digital gold is a vault-stored, 24K, pure gold that users can access via digital platforms like Paytm, PhonePe, GPay, AmazonPay and Groww. Currently, relatively few companies sell digital gold in India. Augmont Goldtech, MMTC-PAMP and SafeGold are the three dominant players. These companies purchase the gold and store them safely in vaults on behalf of the platforms. In contemporary times, some jewelry retailers have ventured into the realm of digital gold investments. This service is provided either through partnerships with established digital gold brands or through the development of in-house platforms. For instance, Tanishq has collaborated with SafeGold to enable their customers to invest in digital gold. Conversely, PC Jewellers has introduced its own platform, named PCJ Digital Gold, to facilitate this form of investment.

This method allows you to invest in small denominations (as low as ₹1 in some cases) making it more accessible to low volume investors.

4. Gold Savings Accounts & Schemes

Select banks offer the option of a Gold Savings Account, which provides a systematic and regular means of investment. It's a safe way to accumulate gold over time. However, the returns from a Gold Savings Account tend to be lower when compared to other investment avenues.

Alternatively, If you already possess physical gold, the Gold Monetization Scheme might be of more interest. It involves depositing your gold with banks in exchange for cash flows as interest on the idle gold. While this option offers a source of income, it comes with a lock-in period and the potential for limited returns.

5. Gold Futures and Options

For those with a higher risk tolerance and trading expertise, gold futures and options can be intriguing. These are traded on commodity exchanges in India, such as the MCX and NCDEX. The advantage here is leverage, which allows you to control a more substantial amount of gold for a fraction of the cost, potentially amplifying gains.

Considering its unique qualities and diversification benefits, incorporating gold into a well-balanced investment portfolio can provide added security and resilience. As investors continue to navigate the dynamic financial landscape, gold's timeless allure and potential for long-term wealth preservation make it a shining star in the realm of investments. However, one should be mindful of the challenges associated with investing in any class of assets, recognizing that even the most ‘riskless’ investment carries risk.

Investor Spotlight

Ramesh Damani – Navigating Market Challenges Amidst Political Tides

By Siddhant Goenka

Ramesh Damani is an Indian ace investor. He primarily invests in Indian and US markets. He rose to fame with his multi-bagger investments in Infosys and CMC.

Ramesh Damani started investing in the markets once his father challenged him to invest $10,000 in the 1980s. During a euphoric bull run in the United States, he lost the entire amount. This event sparked Damani's deep-seated interest in the intricacies of the stock market. Little did he know that this setback would be the catalyst for a lifetime of learning and success. Since then he has amassed a net worth of ₹143 crore.

Damani’s investment philosophy is based on a fundamental principle: choosing the right industry. He meticulously studies market trends, identifying sectors poised for growth and innovation. It's within these fertile grounds that Damani seeks out potential investments. One of his standout successes, Infosys, is a shining example of this approach. In the burgeoning IT industry of the 1980s, Damani recognised the immense potential of technology companies and invested in Infosys as an undervalued pick with reliable management.

Just like Buffett and Munger, who believe in betting big with a few quality stocks, Damani believes in concentration rather than excess diversification Currently, he has only 4 stocks in his portfolio worth ₹143 crores. These are Panama Petrochem, Goldiam International, Valdivarhe Specialty Chemicals and Garden Reach Shipbuilders and Engineering (GRSE), GRSE being his largest investment contributing to ≈70% of his portfolio.

He has invested such a large amount because he has learnt from previous experiences that one needs to back up a good investment thesis with the big bets. His decision to invest in GRSE is underpinned by compelling reasons. GRSE's robust performance, promising future cash flows, and stellar execution capabilities, positions it as a promising entity. Additionally, GRSE's operational efficiency, coupled with its stability evidenced by revenue visibility for up to two years, speaks volumes about its financial strength.

However, Damani is not immune to failures. Damani invested in MTNL and his vision for the company has not panned out. MTNL, once a telecommunications powerhouse, faced a steady decline under the shadow of changing government policies. The policies implemented under the National Democratic Alliance and United Progressive Alliance favored private companies. Then, with the uptrend of 3G and 4G, MTNL started losing market share to private companies and were not able to compete because of bad customer experience as a result of being a monopoly in the industry for the past decade. Damani bought out of this stock quite late and made a heavy loss.

As Damani matured as an investor, he understood the importance of incorporating behavioural finance into his philosophy, which has allowed him the fortune of timing his exits. This keen sense of timing empowers him to safeguard investments during market downturns, positioning himself to buy in when stocks are undervalued. He was able to sense the burst of the dotcom bubble and bought out of Infosys at ₹8,000.

In the world of finance, Damani's wisdom is underscored by his unwavering belief in the power of compounding. He has ardently followed the principle of doubling portfolios every three years, equivalent to a 24% Compound Annual Growth Rate (CAGR).

Ramesh Damani's story serves as a guiding star. His philosophy of selecting promising industries, discerning the right stocks, and mastering the art of timing has led him to remarkable success.

Fundamental Analysis 101: Key Ratios

By Krishna Dixit

Investors use both qualitative and quantitative measures to gauge the financial position and profitability of a company before investing in it. Ratios are an important metric to evaluate various components of a company ranging across profitability, solvency, efficiency and liquidity of a company. Let’s discuss some of the key ratios frequently employed while evaluating a business.

Let’s take a look at the ratios within the context of the two leading consumer products companies of India – Dabur and Marico. Both of them are leading consumer products companies of India with simple businesses and recognisable product portfolios.

1. Return on Invested Capital (and Return on Capital Employed)

Return on Invested Capital (ROIC) assesses a business's profitability and capital efficiency by measuring how it utilises the debt and capital (debt and equity) invested in its core business.

ROIC = EBIT*(1 - tax rate) / Invested Capital

EBIT = NI + Interest + Taxes

Invested Capital = Book value of Debt** + Book value of Equity - Cash - Investments - Other Non-operating Assets

A similar but less stringent measure of a firm’s profitability is the ROCE, which is calculated by dividing EBIT by Capital Employed.

ROCE = EBIT / Capital Employed

Capital Employed = Market value of debt + Market value of Equity

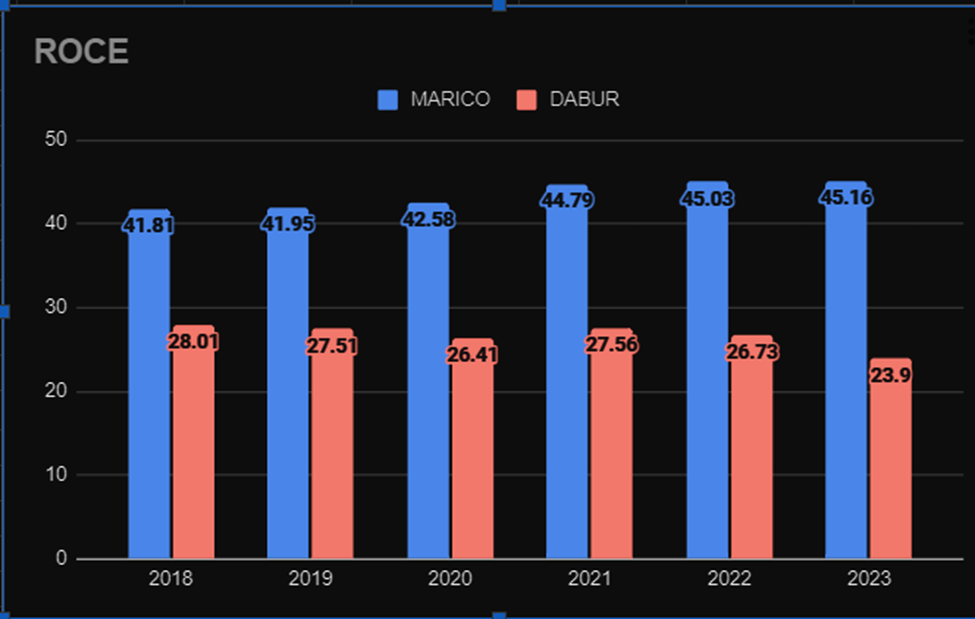

ROCE values can be compared across companies operating within the same sector to gauge their return on their capital. Let’s compare Marico and Dabur’s ROCEs:

For the last 5 years, MARICO’S ROCE has been ranging from 41% to 45%. It means that for every ₹100 of capital, the company generates a return of ₹40. While for Dabur it has been close to around ₹25 for every ₹100 invested as capital. ROCE basically reflects how at what rate the company uses all of its available capital to make money.

** Both long-term and short-term debt

2. Return on Equity

Return on equity (ROE) is a measure of financial performance calculated by dividing net income by shareholders' equity. ROE is also termed as the return on net assets. Return on Equity

ROE = Net Income / Average Shareholders’ Equity

ROE measures the return generated by the company on shareholders’ equity. It measures how well the company uses its share capital to make money for its owners.

Marico’s ROE is close to 38% over the last 5 years, while it is around 25% for Dabur. We can easily infer that for every ₹100 invested in the shares of Marico, the company has generated close to ₹38 for its shareholders.

Important tip: A high ROE might not always be a good indicator of a firm’s profitability and long-term solvency. A company might have a high ROE if it is using a lot of debt in its capital structure, so always check a company’s DE ratio as well.

3. Asset Turnover Ratio

Asset turnover ratio is the ratio between the value of a company’s sales and the value of its assets. The asset turnover ratio can be used as an indicator of the efficiency with which a company is using its assets to generate revenue.

Asset turnover = Net Sales / Total Assets

Both of these companies have been maintaining Asset Turnover ratios greater than 1. Therefore for every ₹1 of assets employed in the business the company is able to churn more in sales. For every ₹100 worth of assets, Marico is able to sell ₹170 of goods. For Dabur, this figure is close to ₹105.

A low asset turnover ratio generally signals issues such as excess production capacity, ineffective inventory management, and inefficient tax collection methods. The higher the asset turnover ratio, the better the company is performing.

4. Debt to Equity Ratio

Debt to Equity essentially gives us the mix of debt and equity employed by the company in its total capital. Forming a part of the solvency ratio, it measures the capital mix of a company. It is a measure of the degree to which a company is financing its operations with debt rather than its own resources.

Debt to Equity = Total Liabilities / Total Shareholder’s Capital

Marico’s debt to equity ratio hovers around 0.12 which means that out of ₹100 invested, only ₹12 is financed through debt. The same is the case for Dabur. These values give a break up of the capital of the company and their reliance on shareholder’s equity to finance their operations. The business seems risk free on the part of debt payments and debt defaults.

A high D/E ratio is often associated with high investment risk; it means that a company relies primarily on debt financing. However, the debt component is a tax deductible expense, therefore, it reduces the tax obligation and expands the money available, which can be utilized for reinvestment of dividend payments. There is no ideal Debt to Equity value for a company, it is a function of the sector it operates in, the cash cycles and business model.

If you’d like to calculate these ratios on your own (which is always a good idea rather than solely relying on analyst reports), head to the websites of Marico and Dabur, go to the investors section, and download the Annual Reports. You can find all the relevant information for calculating these ratios on the Consolidated Balance Sheet and the Consolidated Statement of Profit and Loss (or Income Statement).

Finance Fact

Asia’s Oldest Stock Exchange

By Subham Sen

It's a lesser-known fact that the Bombay Stock Exchange (BSE), famous for its index Sensex, holds the distinction of being not just India's but also Asia's oldest stock exchange. This stretches back to an era when Mumbai, presently recognised as the financial capital, was on the cusp of becoming India's foremost trading hub in the mid-1800s.

In 1855, a group of passionate stockbrokers decided to formalize their trading activities, which had been conducted informally under a banyan tree. This led to the establishment of The Native Share & Stock Brokers Association in 1875. They set up their first formal trading floor in the Dalal Street area of Mumbai.

The establishment of the National Stock Exchange (NSE), renowned as India's most technologically advanced stock exchange, ushered in the era of electronic trading. While this innovation did result in a reduced market share for the BSE, the BSE's enduring legacy, intertwined with India's economic progress and prosperity, has ensured its continued presence as one of the two major stock exchanges in India.