Banking, Holding Companies, and Pulak Prasad

Personal finance, investment philosophies and fun facts - all without the jargon.

Welcome to the eighth edition of the Bodhi Newsletter! In today’s edition, we cover:

Part 2: A Primer on Banking

What is a Holding Company Discount?

Investor Spotlight: Pulak Prasad

Part 2: A Primer on Banking

By Soham Dengra

“Be Fearful When Others Are Greedy and Greedy When Others Are Fearful.”

- Warren Buffet

In the first part of this article, we discussed how a bank makes money, along with some key terms which one should know while analysing the banking sector.

In this article, we’ll understand why banking stocks haven't rallied even in this bull market and what problems are plaguing the banking sector right now.

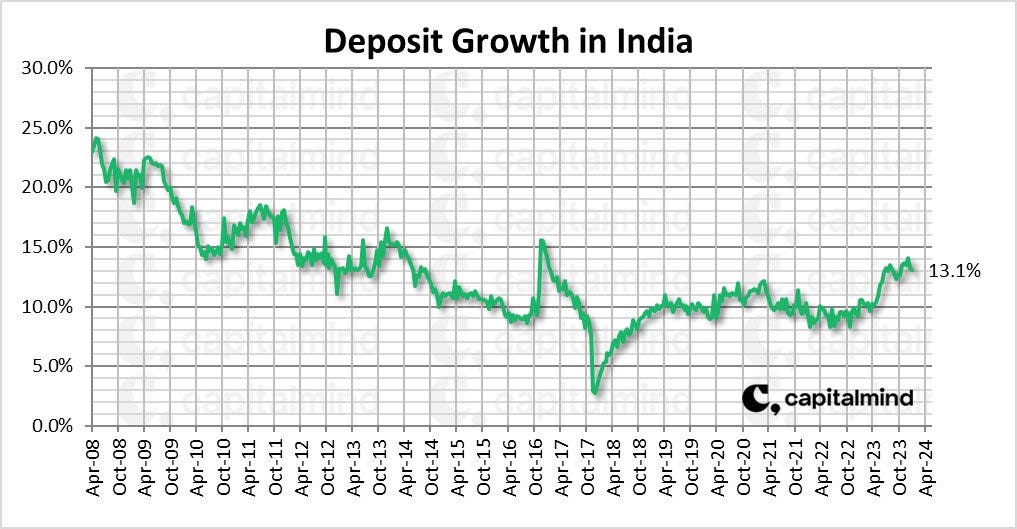

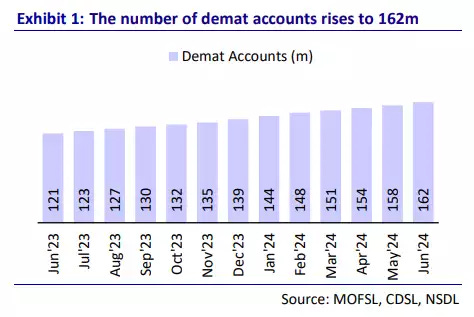

Slow Deposit Growth- Since the last few years, the trend of financialisation has caught pace in India with more and more people deciding to shift their savings from a traditional bank deposit to high-yielding areas like equities and mutual funds. This shift in consumer behaviour is reflected in the large amount of new demat accounts being opened in India and has become a cause for concern for banks as they are now struggling to gather enough deposits. To secure these deposits, banks have had to make these deposits more attractive by increasing the interest rates on their deposits, which is causing a contraction in their Net Interest Margins(NIM).

High Credit-Deposit Ratio- The issue of slow deposit growth goes on to manifest itself into another problem for banks- a high credit-deposit ratio. The nation’s largest banks are battling with high credit deposit ratios which the RBI wants to bring under control to prevent any potential liquidity issues in the sector. While the RBI hasn’t put any hard limit on the credit-deposit ratio for banks, it has been nudging the sector to bring down its CD ratio to around 70-80%. This doesn't auger well for the short-term prospects of the banking sector as it means that banks may have to slow down their lending till their CD ratio lowers, hurting their profitability in the near term.

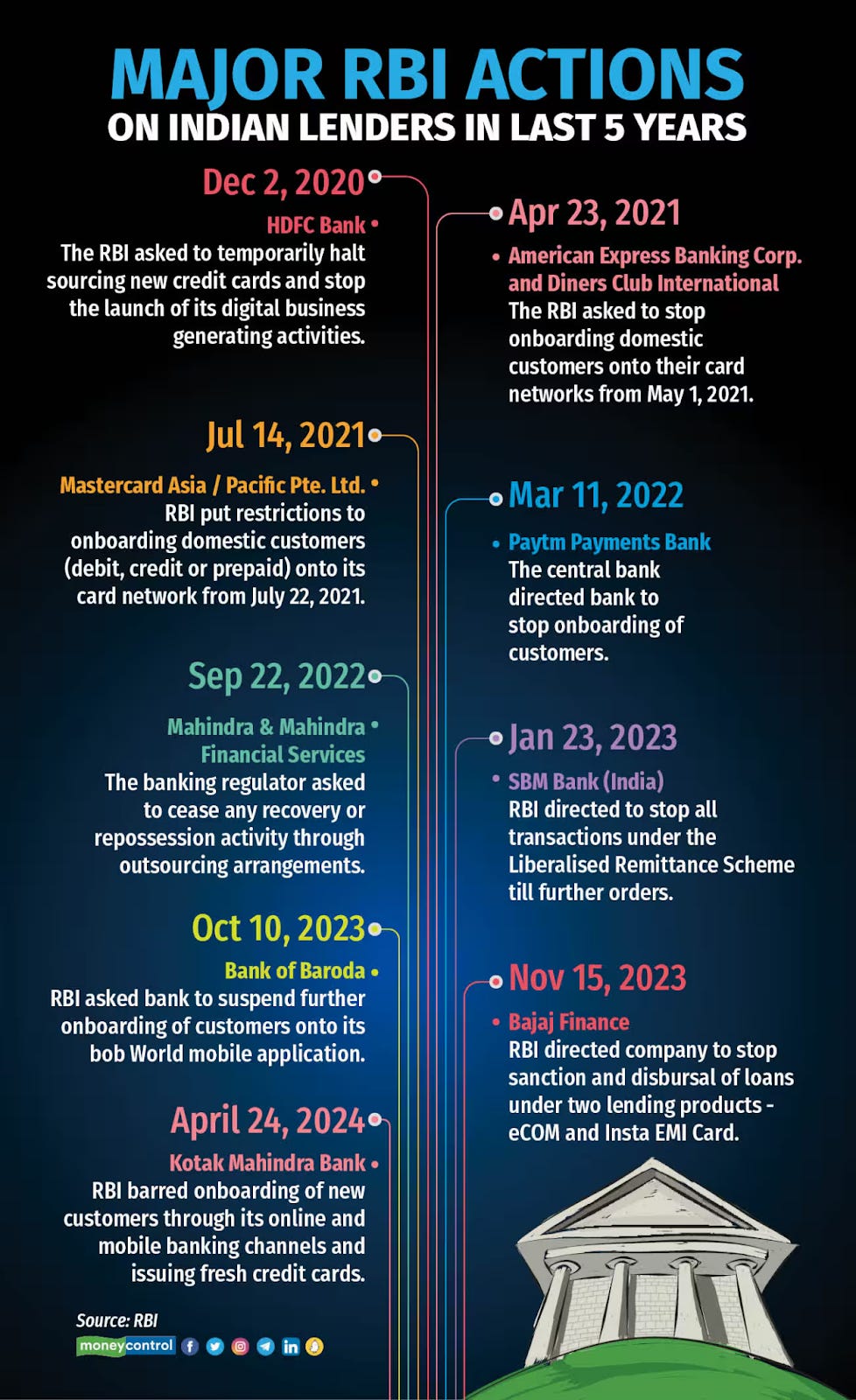

Regulatory Overhang- Since the last few years, the RBI has become much more stringent with its regulation of the Indian banking sector and has issued a slew of fines, bans, and penalties to many small and large banking institutions in the country. A few significant regulatory actions taken by the RBI in the recent past include the temporary ban on the issuance of credit cards by HDFC and Kotak Mahindra Bank; the ban on Paytm Payments Bank; the ban on gold loan issuance by IIFL Finance etc. Apart from these regulatory actions, the central bank has also cracked down on the exponential rise in unsecured retail lending and p2p lending. This heightened stringency and regulatory crackdown has negatively affected the perception around the Indian BFSI stocks, causing a comparative lull in the sector’s performance on the Indian bourses.

So is it a bad time to invest in the Indian Banking sector?

The answer probably depends on your investment horizon. We saw how the sector is facing temporary headwinds which may persist for the next few months, causing a potential drag on the sector’s performance.

However, we also need to keep in mind that Indian banks are in a great financial condition with Non-Performing Assets (NPAs) at record low levels, indicating great asset quality. At the same time, many of these banks are currently trading at considerable discounts to their historical valuations, making them a very attractive long-term investment in a market which is overvalued and frothy.

What is a Holding Company Discount?

By Neel Issrani

What is a Holding Company?

A holding company might sound complex, but it’s actually a simple concept. Imagine a company that doesn’t produce or sell products directly but instead owns shares in other companies. This type of company is known as a holding company. For instance, Bajaj Holdings & Investment Ltd. is a prominent example. It doesn’t manufacture vehicles or provide financial services itself but holds substantial stakes in companies like Bajaj Auto and Bajaj Finserv. Holding companies are created to manage and oversee these investments, allowing for strategic control and diversification.

The Details of the Discount:

But here’s where things get interesting: holding companies often trade at a discount. This means the market values them at less than the sum of their parts! Why would a company that owns valuable stakes in other businesses be worth less than the combined value of those stakes?

First, there’s the issue of control. When you invest in a holding company, you’re buying a stake in a basket of companies, but you have little say in how those companies are managed. This can make investors uneasy, pushing down the price. Then there's the concern about double taxation — when dividends are taxed first at the subsidiary level and then again when they’re passed on to the shareholders of the holding company. Add to this the challenges of governance and transparency (not all holding companies are very open about their internal workings) and the often illiquid nature of some of their assets, and you’ve got a recipe for a discount.

Yet, for some investors, this discount is not a drawback but an opportunity. Why? Because there’s a chance that this gap between the holding company's market value and the underlying asset value will narrow over time. In other words, they’re betting that the market will eventually realize that the holding company is worth more than its current price — and they’ll profit from this revaluation.

But that’s not all. Holding companies sometimes engage in mergers, acquisitions, or restructurings that can unlock significant value for their shareholders. Imagine a holding company that decides to sell an underperforming subsidiary or merge two businesses to create a more efficient and profitable entity. Such moves can serve as catalysts, narrowing the discount as the market reacts positively to the potential for better returns.

This is why some investors find holding companies so appealing. They see the discount not as a problem but as an opportunity to buy into a diversified portfolio at a reduced price. It’s like buying a shopping cart filled with goodies but for less than what each item would cost individually. The hope is that, over time, the market will correct this discount, and they’ll benefit from the upside. Additionally, as these holding companies mostly do not have any operations of their own, they give out most of their profits as dividends turning them into high dividends.

Moreover, holding companies often hold stakes in private or unlisted companies that regular investors can’t directly access. This can provide exposure to unique opportunities, such as startups or niche market leaders, that might not yet be listed on the stock exchange.

Of course, not all holding companies are hidden gems. The discount might exist for valid reasons — maybe the company has a history of poor management decisions, or perhaps its structure is too complex for the market to understand easily. That’s why it’s essential to dig deeper. Look for holding companies with strong management teams, transparent governance, and clear strategies for unlocking value. Watch for signs that the discount might narrow — a planned spin-off, a potential merger, or a strategic acquisition could all serve as triggers for a price rally.

So, the next time you come across a holding company trading below its net asset value, consider whether it’s a hidden value or a potential trap. With the right research, you might just find yourself holding on to a winning ticket.

Investor Spotlight

Pulak Prasad

By Kavya Sharma

One of the most distinguished Market Gurus and the founder of Nalanda Capital, Pulak Prasad, is renowned for his steady investing returns. Through his stellar track record, he has garnered $5 billion in Assets Under Management (AUM), generating a high return of 20.3% CAGR.

Nalanda Capital is a Singapore-based company that makes investments in listed Indian stocks. Before founding Nalanda, Pulak spent over eight years as the Managing Director and Co-Head of India at Warburg Pincus and was affiliated with McKinsey in South Africa, India, and the US.

Pulak graduated from IIT Delhi with a degree in engineering and an MBA from IIM Ahmedabad.

Pulak’s philosophy for investing includes knowing your boundaries or circle of competence and learning how to say no as two crucial skills, no matter how appealing the circumstance. Big investors' capacity to turn down opportunities is frequently more crucial than their ability to accept them.

He is both a historian and a student of markets, and adheres to a straightforward rule that was motivated by Warren Buffett: “you shouldn't lose money, and you shouldn't ever forget that rule”. History has shown us that, in the long run, fewer mistakes and higher profits are possible when you reject businesses that are outside of your area of expertise or that you are unfamiliar with. While Pulak notes that turning down nearly everything that is unknown can cost you the chance to miss out on multibaggers, he believes that turning down what he doesn't know is what gives him the advantage. His research indicates that generating higher returns over time can be enhanced by avoiding mistakes and staying true to your knowledge. Gaining an understanding of a business enables investors to ride out ups and downs and value the company regardless of external factors such as globalization, macroeconomic fluctuations, or competition and helps avoid unnecessary diversification.

Another lesson Pulak has derived from Warren Buffett states, "We don't believe in buying stocks; we believe in buying businesses." Pulak has adopted this philosophy. Pulak believes in owning businesses forever, not merely timing the market or treating investments as assets, and he loves to collaborate with excellent managers. Rather than being market timing equity investors, Nalanda Capital seeks to be long-term business owners, functioning as partners as opposed to mere shareholders.

Prior to learning from Charlie Munger, Buffett adhered to Benjamin Graham's theory of purchasing companies below their intrinsic value. However, Pulak, like Buffett, now prefers to purchase high-quality companies at a fair price, particularly in difficult economic circumstances.

Pulak Prasad's investment philosophy centres on deep research and a thorough understanding of the businesses he invests in. He emphasizes investing in companies with a strong competitive advantage and sustainable business models, combining his engineering degree and MBA with extensive market experience. His disciplined approach involves avoiding hype and focusing on intrinsic value, which is reflected in Nalanda Capital’s long-term investment horizon and its focus on companies with robust fundamentals. Under Prasad's leadership, Nalanda Capital has made significant investments in high-profile companies, showcasing his skill in identifying promising opportunities through a rigorous due diligence process. Additionally, Prasad has authored “What I Learned About Investing from Darwin” and given talks on investing, sharing his insights on market trends and investment strategies, which further illustrates his thought leadership in the field.